-

Attention Real Estate and Other Activities Under SUGEF Regulation

SUGEF regulated entities will now have to register at ICD (Instituto Costarricense Sobre Drogas) ICD is the major entity in charge of fighting against the stated in law 8204, the law for the prevention of money laundering, financing terroristm, ilegal wealth building, and related activities. Since the law was created, financial and related entities like…

-

D-101 Form Compliance for Dormant Corporations Has Been Reprogrammed to 2023

November 09th, 2022 The tax administration of Costa Rica has informed today that the owners of dormant corporations that have not complied with the filing of the D-101 form for dormant corporations will now have a time extention to comply until April 30th, 2023. The extension of time to comply with this requirement has been given…

-

Costa Rican Home Owners Listed in Aibnb Will Have To Register As Tax Payers

The Tax Administration of Costa Rica has announced in October that Airbnb has been added to the list of service providers overseas that will be automatically charged 13% VAT tax on every booking processed, this means that guests will now be charted the Tax even if the host of the listing hasn’t included it in…

-

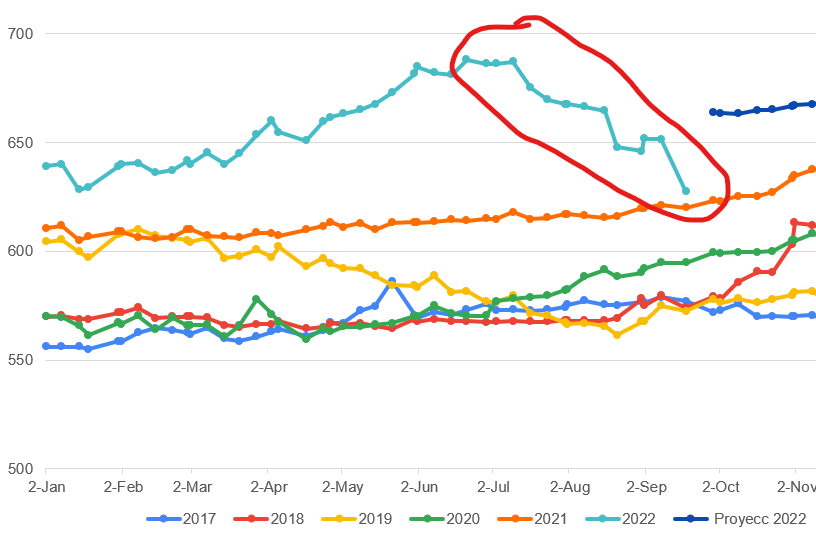

Why The Dollar Vrs Costa Rican Colon Has Decreased Considerably In Last Weeks

Source Central Bank of Costa Rica The reduction from the last weeks in the exchange between the Dollar and the Costa Rican Colon has brought the price very close to the same price of 2021 as of the current date, this is something that will affect the operation of the individuals and companies that make…

-

Costa Rican Government Approved New Hemp (CBD) & Medicinal Cannabis Regulation in Costa Rica

On august 24th, 2022, the Costa Rican president signed the new law 19256 for the regulation of the medical and therapeutic usage of marihuana and hemp in it’s different versions for the alimentary and industrial usage, this law is expected to produce a positive effect in the economy looking for contributing to its reactivation with…

-

Tax On Luxury Homes in Costa Rica

Many of our clients regularly request us information about how what are the brackets that make property owners to be subject to luxury tax for their homes in Costa Rica and what are the rates for it, how should it be declared and how often and other important questions about this tax. For all those…

-

New Deadline Extension (D-101 Form for Inactive Corporations)

Last week, the tax administration informed that they have extended the deadline to comply with the filing of the D-101 form for inactive corporations, now the corporation owners that haven’t complied with this mandatory requirement have until November 15th, 2022 to file this mandatory form. The D-101 Form for inactive corporations, also known as the…

-

Costa Rica Taxes 101

Everything you need to know about taxes in Costa Rica, a summary with the most common facts that any foreign wonder when thinking on doing business here.

-

New Costa Rican Visa For Digital Nomad-Remote Workers

Yes, the new VISA for digital nomads has finally arrived and the regulation has been signed by the president of Costa Rica

-

Update on Cyber Attacks to CR Government

The Tax Office finally figured it out, they have enabled the online portal for filing taxes and they will be in the way to have all their services back online

-

Update On Tax Administration & CCSS Cyber Attacks

Update On Tax Administration and CCSS Cyber Attacks

-

Tax Administration of Costa Rica Hacked by Russian Group

The Tax Office along some other institutions of Costa Rica has been victim of a cyber attack, more information on this post and coming ones

-

Deadline for the new tax form for inactive corporation has been extended for 3 months

The Costa Rican tax administration has extended the deadline date for the D-101 form

-

Tax Brackets By Entity For Fiscal Year 2022

The tax administration has published the new tax brackets for the year 2022, the different tax rates will depend on if your business activity is registered under an individual, a corporation or a salary. The following are the rates for the current fiscal year: In ConsultantsCR we’re accounting, financial, legal and real estate advisors, feel…

-

New tax form for inactive corporations due march 15th, 2022

The original deadline for this requirement was on march 15th 2021, the Tax Admin. has defined March 15th, 2022 as the final deadline for this requirement, with this change corporations that were created before 2022 will need filling this requirement for two fiscal períods (2021-2022) According to the tax Administration, March 15th, 2022 will be…

-

Hiring Staff As Consultant or Employee? What’s Best For My Business?

Consultant or employee? What is the best for business owners to hire their staff in Costa Rica

-

Check Out This Article About #CostaRica

The following post was published by “La Nacion”, a Costa Rican famous paperwork, it shows the progress made by CR in attracting and providing value for foreign investor firms and individuals, you can read the full article in the link below: https://www.nacion.com/economia/indicadores/costa-rica-obtiene-el-primer-lugar-en-el-mundo-por/FW7BDUX7Q5G63AIHEXTL23GXAY/story/?outputType=amp-type

-

Is Costa Rica A Fiscal Paradise?

in this post we discover some of the hidden attractions of Costa Rica as a tax paradise, it might not be in the list of tax heavens but there are definitely some interesting facts about their policies

-

Leasing or Renting? What’s Better for Tax Purposes?

What are the advantages of having a leasing or a renting a vehicle in Costa Rica, what are the best options for tax purposes. in ConsultantsCR we advise about those two forms of leasing an asset

-

All About MEIC – What Are The Benefits Of Registering Your Company

MEIC is the ministry of economics and commerce in Costa Rica, we explain how you can get tax benefits from having your corporation registered